Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

How to Handle Multiple Offers on Your Home

HOW TO HANDLE

Multiple Offers on Your Home

Handling multiple offers on your home can be exhilarating and daunting. Here’s how to make the best choice.

Evaluate Each Offer Carefully

When you receive multiple offers, resist the urge to rush into a decision based solely on the highest bid. Take the time to thoroughly review each offer, considering the following factors:

Offer Price

Compare the offered prices against your asking price and recent comparable sales in your area.

Financial Qualifications

Evaluate the financial strength of each buyer. Offers backed by pre-approved financing or cash tend to be more secure.

Earnest Money Deposit

Consider the amount of earnest money offered as it reflects the buyer’s commitment to the purchase.

Contingencies

Review the contingencies outlined in each offer, such as financing, appraisal, inspection, and sale of buyer’s property.

Closing Timeline

Assess proposed closing dates and determine if they align with your needs.

Additional Terms

Look for any special terms or requests that may impact the sale, such as seller concessions or specific repair requests.

Consider More Than Just Price

While the price offered is a crucial consideration, it’s important to look beyond dollars and cents.

A high offer may initially seem attractive, but the overall terms and conditions attached to each offer can significantly influence its desirability and the level of risk involved.

Create a Deadline

Setting a deadline for submitting offers is crucial in the home-selling process. It creates urgency among potential buyers and submit their best offers promptly.

This urgency encourages buyers to carefully consider their offer terms and present competitive bids, streamlining the decision-making process for the seller.

Communicate Clearly

Maintaining transparent communication with all parties involved is crucial during the negotiation process.

Clearly articulating your expectations, timelines, and any counteroffers helps prevent misunderstandings and missed opportunities. Proactive communication fosters trust and efficiency in the transaction, ensuring a smooth and successful sale.

Seek Professional Guidance

Leveraging the expertise of your real estate agent is invaluable when handling multiple offers. Your agent can provide valuable insights, negotiate on your behalf, and offer guidance based on current market trends and local conditions.

Their experience can help you navigate complexities and identify the most advantageous offer for your specific circumstances.

Make a Decision

After carefully evaluating and considering all offers, it’s crucial to select the one that aligns best with your goals, timeline, and financial expectations. This decision should be made thoughtfully to ensure a successful transaction. Respond promptly to accepted offers to maintain momentum and facilitate a smooth transition toward closing. Timely communication helps build trust and reliability with the buyer, fostering a positive and efficient selling experience overall.

Conclusion

Navigating multiple offers can be both exciting and overwhelming, but with a thoughtful approach, you can turn this situation into a major advantage. By weighing more than just the offer price—factoring in financial strength, contingencies, and closing terms—you position yourself to make the most strategic decision. Lean on your real estate agent’s expertise, communicate clearly, and stay focused on your goals. The right offer isn’t always the highest—it’s the one that brings you the most value and peace of mind as you move on to your next chapter.

Need real estate advice?

Feel free to reach out; I would love to help you wherever you are on your real estate journey.

Should We Wait for Rates to Drop?

Everyone keeps asking if they should wait for rates to drop.

Here’s the reality and some context:

In the 1980s, people were buying homes at 12%

In 2020, rates were around 3%

Today we’re in the mid 6% range

In 2025 the average was 6.6%

Today it’s just a touch lower.

People think waiting is the “safe” move. Just hang tight until rates come down and then jump in. Sounds logical, but what usually gets missed is what happens when that plays out.

If rates drop, more buyers come back into the market. Demand picks up. Competition gets tighter. Prices tend to move up again.

Some price ranges are seeing more competition than others so you may still experience stiffer competition especially if the homes are in good condition and in a gret location.

Not encouraging anyone to do anything just trying to provide some context.

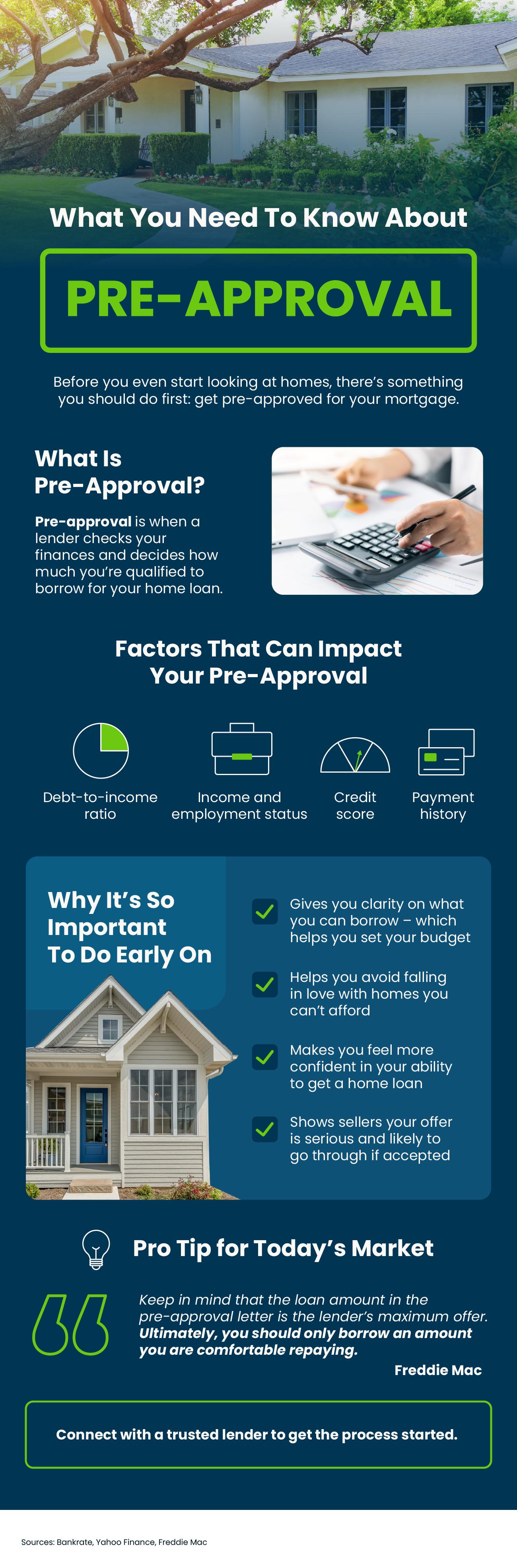

What You Need To Know About Pre-Approval

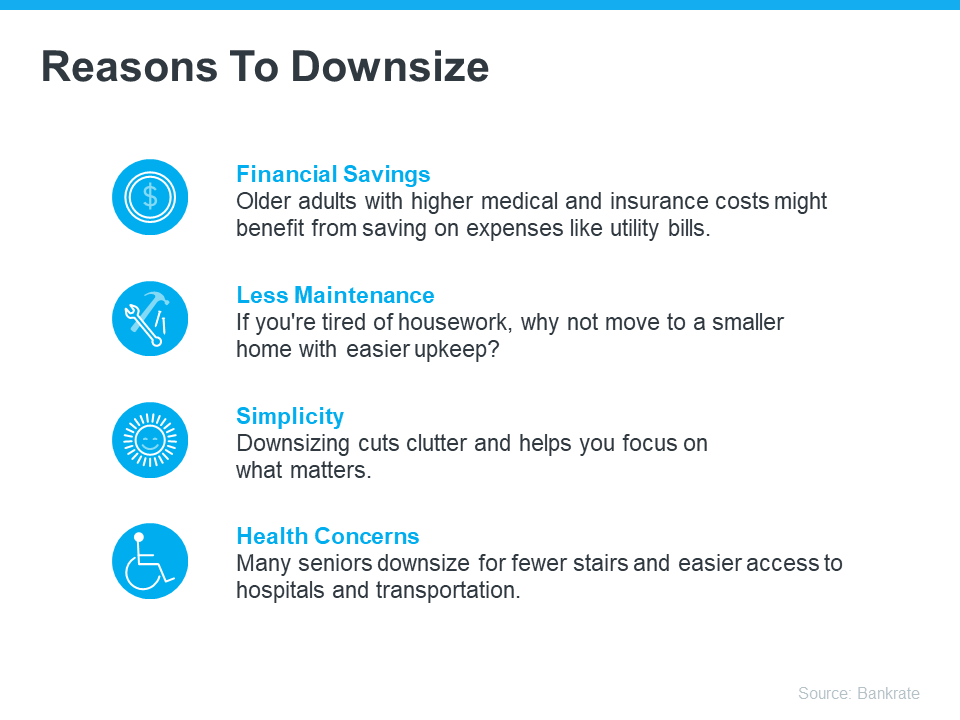

Why Moving to a Smaller Home After Retirement Makes Life Easier

Why Moving to a Smaller Home After Retirement Makes Life Easier

Retirement is a time for relaxation, adventure, and enjoying the things you love. As you imagine this exciting new chapter in your life, it’s important to think about whether your current home still fits your needs.

If it’s too big, too costly, or just not convenient anymore, downsizing might help you make the most of your retirement years. To find out if a smaller, more manageable home might be the perfect fit for your new lifestyle, ask yourself these questions:

- Do the original reasons I bought my current house still stand, or have my needs changed since then?

- Do I really need and want the space I have right now, or could somewhere smaller be a better fit?

- What are my housing expenses right now, and how much do I want to try to save by downsizing?

If you answered yes to any of these, consider the benefits that come with downsizing.

The Benefits of Moving into a Smaller Home

There are many reasons why you should downsize. Here are just a few from Bankrate:

Your Equity Can Help Make Downsizing Possible

If those perks sound like something you’d want, you may already have what you need to make it happen. A recent article from Seniors Guide shares:

“And at a time when homeowners age 62 and older have more than $12 trillion in home equity, downsizing makes sense . . .”

If you’ve been in your house for a while, odds are you’re one of those homeowners who’s built up a considerable amount of equity. And that equity is something you can use to help you buy a home that better fits your needs today. Greg McBride, Chief Financial Analyst at Bankrate, explains:

“Downsizing can mean taking that equity when the home is sold and using it to pay cash or make a large down payment on a lower-priced home, reducing your monthly living expenses.”

When you’re ready to use all that equity to fuel your next move, your real estate agent will be your guide through every step of the process. That includes setting the right price for your current house when you sell, finding the home that best fits your evolving needs, and understanding what you can afford at today’s mortgage rate.

Bottom Line

Starting your retirement journey? Think about downsizing – it could really help. When you’re ready, let’s connect.

Do Elections Impact the Minneapolis Area Housing Market?

Do Elections Impact the Housing Market?

The 2024 Presidential election is just months away. As someone who’s thinking about potentially buying or selling a home, you’re probably curious about what effect, if any, elections have on the housing market.

It’s a great question because buying or selling a home is a major decision, and it’s natural to wonder how such a major event might impact your plans.

Historically, Presidential elections have only had a small, temporary impact on the housing market. Here’s the latest on exactly what’s happened to home sales, prices, and mortgage rates throughout those time periods.

Home Sales

During the month of November, in years when the Presidential election takes place, there’s typically a slight slowdown in home sales. As Ali Wolf, Chief Economist at Zonda, explains:

“Usually, home sales are unchanged compared to a non-election year with the exception being November. In an election year, November is slower than normal.”

This is mostly because some people feel uncertain and hesitant about making big decisions during such a pivotal time. However, it’s important to know this slowdown is temporary. Historically, home sales bounce back in December and continue to rise the following year.

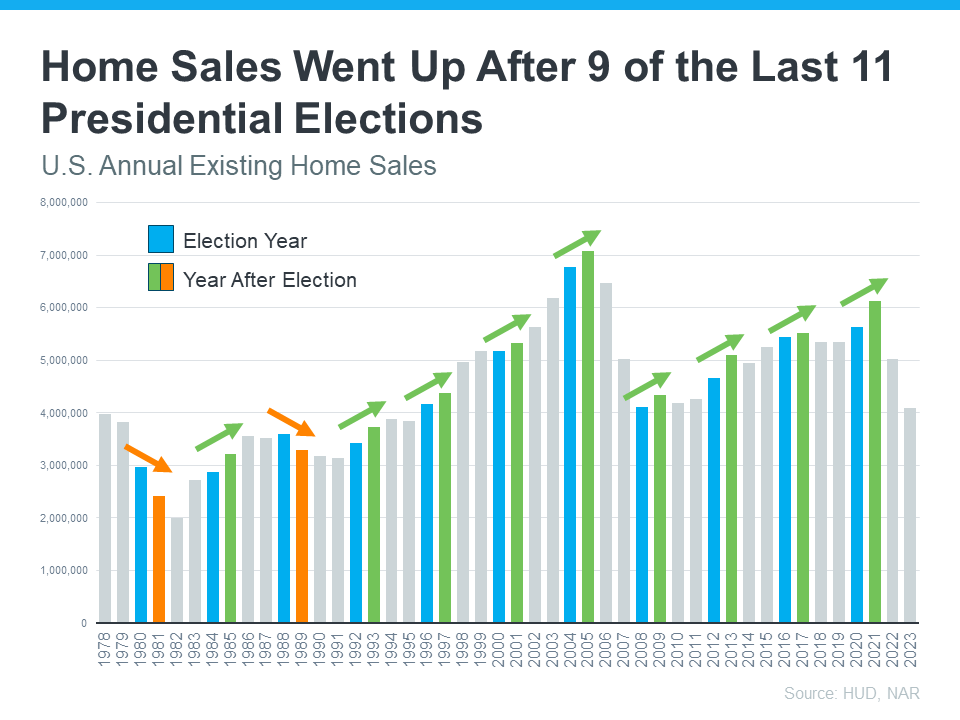

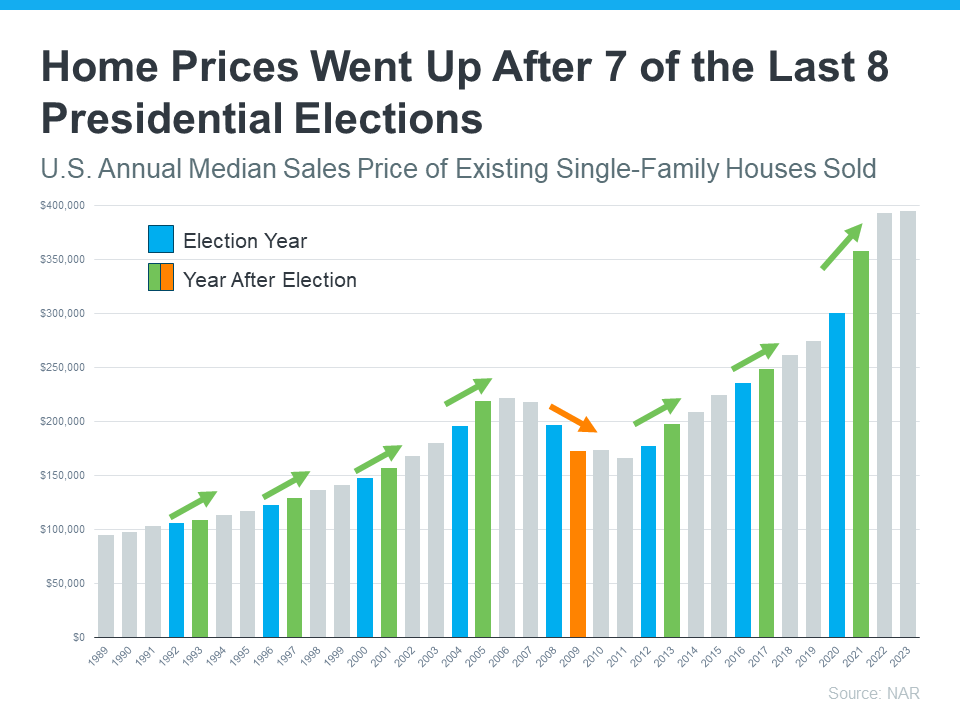

In fact, data from the Department of Housing and Urban Development (HUD) and the National Association of Realtors (NAR) shows after nine of the last 11 Presidential elections, home sales went up the next year (see graph below):

The graph shows annual home sales going back to 1978. Each year with a Presidential election is noted in blue. The year immediately after each election is green if existing home sales rose that year. The two orange bars represent the only years when home sales decreased after an election.

Home Prices

What about home prices? Do they drop during election years? Not typically. As residential appraiser and housing analyst Ryan Lundquist puts it:

“An election year doesn’t alter the price trend that is already happening in the market.”

Home prices are pretty resilient. They generally rise year-over-year, regardless of elections. The latest data from NAR shows after seven of the last eight Presidential elections, home prices increased the following year (see graph below):

Just like the previous graph, this shows election years in blue. The only year when prices declined after an election is in orange. That was during the housing market crash, which was far from a typical year. Today’s market is different than it was back then.

All the green bars represent when prices rose the following year. So, if you’re worried about your home losing value because of an election, you can rest easy knowing prices rise after most Presidential elections.

Mortgage Rates

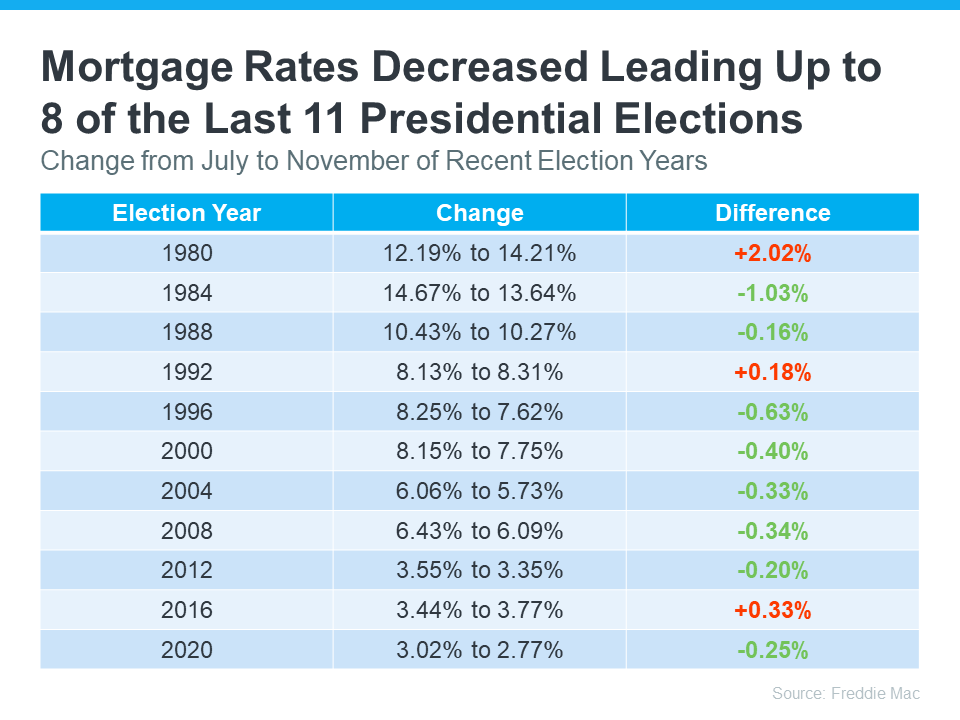

Mortgage rates are important because they affect how much your monthly payment will be when you buy a home. Looking at the last 11 Presidential election years, data from Freddie Mac shows mortgage rates decreased from July to November in eight of them (see chart below):

Most forecasts expect mortgage rates to ease slightly throughout the remainder of the year. If they’re right, this year will follow the trend of declining rates leading up to most previous elections. And if you’re looking to buy a home in the coming months, this could be good news, as lower rates could mean a lower monthly payment.

What This Means for You

So, what’s the big takeaway? While Presidential elections do have some impact on the housing market, the effects are usually small and temporary. As Lisa Sturtevant, Chief Economist at Bright MLS, says:

“Historically, the housing market doesn’t tend to look very different in presidential election years compared to other years.”

For most buyers and sellers, elections don’t have a major impact on their plans.

Bottom Line

While it’s natural to feel a bit uncertain during an election year, history shows the housing market remains strong and resilient. For help navigating the market, election year or not, let’s connect.

The 2024 Presidential election is just months away. As someone who’s thinking about potentially buying or selling a home, you’re probably curious about what effect, if any, elections have on the housing market.

It’s a great question because buying or selling a home is a major decision, and it’s natural to wonder how such a major event might impact your plans.

Historically, Presidential elections have only had a small, temporary impact on the housing market. Here’s the latest on exactly what’s happened to home sales, prices, and mortgage rates throughout those time periods.

Home Sales

During the month of November, in years when the Presidential election takes place, there’s typically a slight slowdown in home sales. As Ali Wolf, Chief Economist at Zonda, explains:

“Usually, home sales are unchanged compared to a non-election year with the exception being November. In an election year, November is slower than normal.”

This is mostly because some people feel uncertain and hesitant about making big decisions during such a pivotal time. However, it’s important to know this slowdown is temporary. Historically, home sales bounce back in December and continue to rise the following year.

In fact, data from the Department of Housing and Urban Development (HUD) and the National Association of Realtors (NAR) shows after nine of the last 11 Presidential elections, home sales went up the next year (see graph below):

The graph shows annual home sales going back to 1978. Each year with a Presidential election is noted in blue. The year immediately after each election is green if existing home sales rose that year. The two orange bars represent the only years when home sales decreased after an election.

Home Prices

What about home prices? Do they drop during election years? Not typically. As residential appraiser and housing analyst Ryan Lundquist puts it:

“An election year doesn’t alter the price trend that is already happening in the market.”

Home prices are pretty resilient. They generally rise year-over-year, regardless of elections. The latest data from NAR shows after seven of the last eight Presidential elections, home prices increased the following year (see graph below):

Just like the previous graph, this shows election years in blue. The only year when prices declined after an election is in orange. That was during the housing market crash, which was far from a typical year. Today’s market is different than it was back then.

All the green bars represent when prices rose the following year. So, if you’re worried about your home losing value because of an election, you can rest easy knowing prices rise after most Presidential elections.

Mortgage Rates

Mortgage rates are important because they affect how much your monthly payment will be when you buy a home. Looking at the last 11 Presidential election years, data from Freddie Mac shows mortgage rates decreased from July to November in eight of them (see chart below):

Most forecasts expect mortgage rates to ease slightly throughout the remainder of the year. If they’re right, this year will follow the trend of declining rates leading up to most previous elections. And if you’re looking to buy a home in the coming months, this could be good news, as lower rates could mean a lower monthly payment.

What This Means for You

So, what’s the big takeaway? While Presidential elections do have some impact on the housing market, the effects are usually small and temporary. As Lisa Sturtevant, Chief Economist at Bright MLS, says:

“Historically, the housing market doesn’t tend to look very different in presidential election years compared to other years.”

For most buyers and sellers, elections don’t have a major impact on their plans.

Bottom Line

While it’s natural to feel a bit uncertain during an election year, history shows the housing market remains strong and resilient. For help navigating the market, election year or not, let’s connect.

Home Prices Aren’t Declining, But Headlines Might Make You Think They Are!

Home Prices Aren’t Declining, But Headlines Might Make You Think They Are

If you’ve seen the news lately about home sellers slashing prices, it’s a great example of how headlines do more to terrify than clarify. Here’s what’s really happening with prices.

The bottom line is home prices are higher than they were a year ago at this time, and they’re expected to keep rising, just at a slower pace.

But a recent article from Redfin notes,

“Price Drops Hit Highest Level in 18 Months As High Rates Dampen Buyer Demand.”

And that might make you think prices are declining.

Now, while it’s true the latest report from Realtor.com also shows 16.6% of homes on the market had price reductions in May, which is up from 12.7% last May, that doesn’t mean overall home prices are falling.

The key is knowing the difference between the asking price and the sold price.

Understanding Asking Price vs. Sold Price

In essence, the asking price, also known as a listing price, is the amount a seller hopes to get for their home when they list it. In reality, sellers can’t just put any price tag on their house and expect it to sell for top dollar. Today’s buyers are savvy customers, and when they aren’t willing to pay a premium for a home because their budgets are strained by higher mortgage rates, sellers need to adjust. And that’s what’s happening right now.

Based on market factors and what offers that seller receives, that asking price can change. If a seller isn’t getting much foot traffic, you may see them revise the price and make an adjustment to reignite interest in the home – and sometimes that’s because they’ve overpriced it from the start. That’s where price reductions come in, and when you see “price drops” in a headline, it sounds like declining home prices.

Mike Simonsen, CEO and Founder of Altos Research, says:

“Not only is the share of homes with price cuts elevated compared to one year ago, but more price cuts are happening each week than last year.”

On the other hand, the final sold price is the amount a buyer actually pays when the transaction is complete.

Here’s the most important thing to note: Actual sold prices are still rising, and they’re expected to continue to do so at least over the next 5 years.

What Does This Mean for Home Prices?

So, while there’s been an increase in price reductions recently, this doesn’t mean overall home values are declining. Instead, it’s a sign that demand is moderating. And, as a result, sellers are adjusting their expectations to align with today’s market reality.

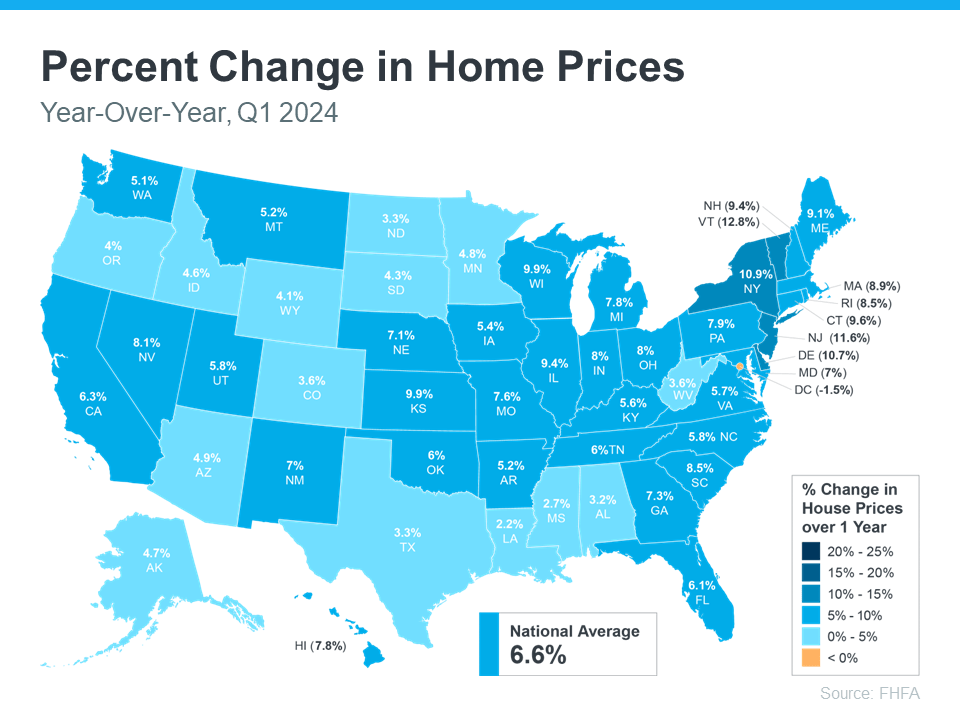

Even with more price reductions, home values are still growing on an annual basis, as they do nearly every year in the housing market. According to the Federal Housing Finance Agency (FHFA), home prices went up 6.6% over the last year (see below):

This map shows how prices rose just about everywhere in the country, indicating the market is not in decline.

So, while seller price reductions are often a leading indicator that prices may moderate in the months ahead, which experts have been saying for a while is expected to happen, they aren’t necessarily reason for alarm. The same article from Redfin also states:

“. . .those metrics suggest sale-price growth could soften in the coming months as persistently high mortgage rates turn off homebuyers. For now, the median-home sale price is up 4.3% year over year to another record high. . .”

And with inventory as tight as it is today, price moderation is much more likely in upcoming months than price declines.

Why This Is Good News for Buyers and Sellers

For buyers, more realistic asking prices mean a better chance of securing a home at a fair price. It also means you can enter the market with more confidence, knowing prices are stabilizing rather than continuing to skyrocket.

For sellers, understanding the need to adjust your asking price can lead to faster sales and fewer price negotiations. Setting a realistic price from the start can attract more serious buyers and lead to smoother transactions.

Bottom Line

While the uptick in price reductions might seem troubling, it’s not a cause for concern. It reflects a market adjusting to new conditions. Home prices are continuing to grow, just at a more moderate pace.

Focus on Time in the Market, Not Timing the Market

Focus on Time in the Market, Not Timing the Market

Should you buy a home now or should you wait? That’s a big question on many people’s minds today. And while what timing is right for you will depend on a lot of other personal factors, here’s something you may not have considered.

If you’re able to buy at today’s rates and prices, it may be better to focus on time in the market, rather than timing the market.

The Downside of Trying To Time the Market

Trying to time the market isn’t a good strategy because things can change. Here’s an example. For the better part of this year, projections have said mortgage rates will come down. And while experts agree that’s still what’s ahead, shifts in various market and economic factors have pushed back the timing of when that’ll happen. Here’s how that’s impacted homebuyers who’ve been sitting on the sidelines. As U.S. News says:

“Those who put off buying a home during the past few years as they were holding out for lower mortgage rates have been left out of the market . . . mortgage rates have stayed higher for longer than previously expected, keeping monthly housing payments elevated. In other words, affordability didn’t improve for those who chose to wait.”

This is why timing the market may not pay off if you’re ready and able to buy now.

The Proof Is in the Pudding: How Homeowners Benefit from Rising Home Prices

Delaying your plans also means missing out on the equity you’d gain if you went ahead with your purchase today. And the potential equity gains that are at stake may surprise you.

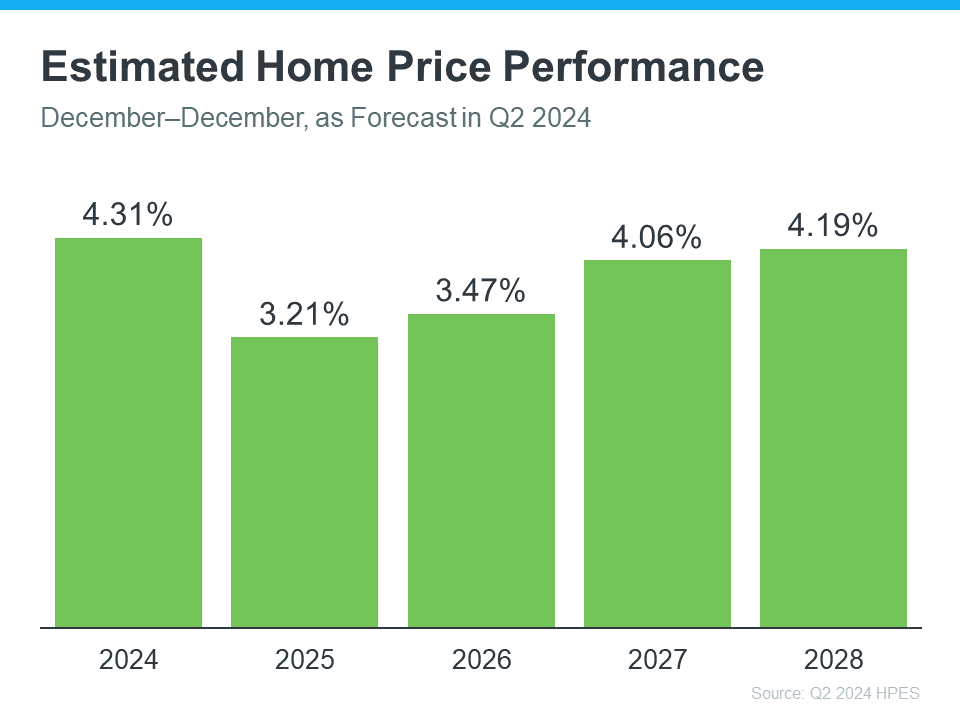

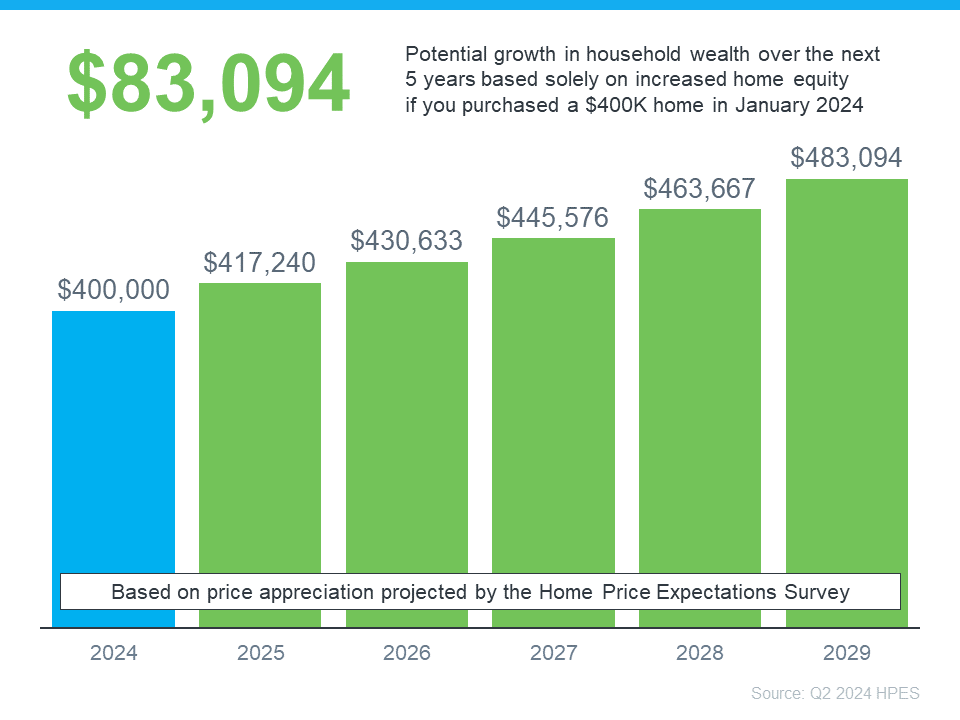

Each quarter, Fannie Mae releases the Home Price Expectations Survey. It asks over one hundred economists, real estate experts, and investment and market strategists what they forecast for home prices over the next five years. In the latest release, experts are projecting home prices will continue to rise through at least 2028 (see the graph below):

To give these numbers context, let’s take a look at a breakdown of what you stand to gain once you buy. The graph below uses a typical home’s value to show how a home could appreciate over the next few years using those HPES projections:

In this example, let’s say you went ahead and bought a $400,000 home at the beginning of this year. Based on the expert forecasts from the HPES, you could gain more than $83,000 in household wealth over the next five years. That’s not a small number.

This data helps paint the picture of why time in the market really matters.

The Advice You Need To Hear If You’re Ready and Able To Buy Now

Right now, you may be focused on what’s happening with mortgage rates and how those impact your monthly payment, but don’t forget to factor in home prices.

Prices are expected to continue climbing, just at a more moderate pace. And while a moderate rise in prices may not be fun for you now, once you own a home, that growth will be a huge perk. That’s the time in the market piece.

Sure, you could try timing the market, but the equity you’ll be missing out on in the meantime is something to seriously consider. If you’re ready and able to buy now, you have to decide: is it really worth waiting?

Rather than focusing on timing the market. It’s better to have time in the market.

As U.S. News Real Estate sums up:

“There’s never a one-size-fits-all answer to whether now is the right time to buy a home. . . . There’s also no way to predict precisely what the market will do in the near future . . . Perfectly timing the market shouldn’t be the goal. This decision should be determined by your personal needs, financial means and the time you have to find the right home.”

Bottom Line

If you’re debating whether to buy now or wait, remember it’s time in the market, not timing the market. And if you want to get the ball rolling and set yourself up for those big equity gains, let’s connect to make it happen.

Outdoor Upgrades to Wow Homebuyers

Want to move, but trying to decide what to tackle before selling?

Let’s connect to go over the best ways to spend your time and money.

Ways To Use Your Minnesota Tax Refund If You Want To Buy a Home

Ways To Use Your Tax Refund If You Want To Buy a Home

Have you been saving up to buy a home this year? If so, you know there are a number of expenses involved – from your down payment to closing costs. But did you also know your tax refund can help you pay for some of these expenses? As Credit Karma explains:

“If one of your goals is to stop renting and buy a home, you’ll need to save up for closing costs and a down payment on the mortgage. A tax refund can give you a start on the road to homeownership. If you’ve already started to save, your tax refund could move you down the road faster.”

While how much money you may get in a tax refund is going to vary, it can be encouraging to have a general idea of what’s possible. Here’s what CNET has to say about the average increase people are seeing this year:

“The average refund size is up by 6.1%, from $2,903 for 2023’s tax season through March 24, to $3,081 for this season through March 22.”

Sounds great, right? Remember, your number is going to be different. But if you do get a refund, here are a few examples of how you can use it when buying a home. According to Freddie Mac:

- Saving for a down payment – One of the biggest barriers to homeownership is setting aside enough money for a down payment. You could reach your savings goal even faster by using your tax refund to help.

- Paying for closing costs – Closing costs cover some of the payments you’ll make at closing. They’re generally between 2% and 5% of the total purchase price of the home. You could direct your tax refund toward these closing costs.

- Lowering your mortgage rate – Your lender might give you the option to buy down your mortgage rate. If affordability is tight for you at today’s rates and home prices, this option may be worth exploring. If you qualify for this option, you could pay upfront to have a lower rate on your mortgage.

The best way to get ready to buy a home is to work with a team of trusted real estate professionals who understand the process and what you’ll need to do to be ready to buy.

Bottom Line

Your tax refund can help you reach your savings goal for buying a home. Let’s talk about what you’re looking for, because your home may be more within reach than you think.

Overpricing Your House Could Cost You

Why Overpricing Your House Can Cost You

If you’re trying to sell your house, you may be looking at this spring season as the sweet spot – and you’re not wrong. We’re still in a seller’s market because there are so few homes for sale right now. And historically, this is the time of year when more buyers move. Competition ticks up. That makes this an exciting time to put up that for sale sign.

But while conditions are great for sellers like you, I still want you to be strategic when it comes time to set your asking price. That’s because pricing your house too high may actually cost you in the long run.

The Downside of Overpricing Your House

The asking price for your house sends a message to potential buyers. From the moment they see your listing, the price and the photos are what’s going to make the biggest first impression. And, if it’s priced too high, you may turn people away. They may not even consider seeing your home ‘in person’. As an article from U.S. News Real Estate says:

“Even in a hot market where there are more buyers than houses available for sale, buyers aren’t going to pay attention to a home with an inflated asking price.”

That’s because no homebuyer wants to pay more than they have to, especially not today. Many are already feeling the pinch on their budget due to ongoing home price appreciation and today’s mortgage rates. And if they think your house is overpriced, they may write it off without even stepping foot in the front door, or simply won’t make an offer if they think it’s priced too high.

If that happens, it’s going to take longer to sell. And ideally you don’t want to have to think about doing a price drop to try to re-ignite interest in your house. Why? Some buyers will see the price cut as a red flag and wonder why the price was reduced. Or they’ll think something is wrong with the house the longer it sits. As an article from Forbes explains:

“It’s not only the price of an overpriced home that turns buyers off. There’s also another negative component that kicks in. . . . if your listing just sits there and accumulates days on the market, it will not be a good look. . . . buyers won’t necessarily ask anyone what’s wrong with the home. They’ll just assume that something is indeed wrong, and will skip over the property and view more recent listings.”

Your Agent’s Role in Setting the Right Price

Instead, pricing it at or just below current market value from the start is a much better strategy. So how do you find that ideal asking price? You lean on the pros. Only an agent has the expertise needed to research and figure out the current market value for your home.

I’ll factor in the condition of your house, any upgrades you’ve made, and what other houses like yours are selling for in your area. And I’ll use all of that information to find that target number. The right price will bring in more buyers and make it more likely you’ll see multiple offers too. Plus, when homes are priced right, they still tend to sell quickly.

Bottom Line

Even though you want to bring in top dollar when you sell, setting the asking price too high may deter buyers and slow down the sales process.

Let’s connect to find the right price for your house, so we can maximize your profit and still draw in eager buyers willing to make competitive offers.