Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

Outdoor Upgrades to Wow Homebuyers

Want to move, but trying to decide what to tackle before selling?

Let’s connect to go over the best ways to spend your time and money.

Ways To Use Your Minnesota Tax Refund If You Want To Buy a Home

Ways To Use Your Tax Refund If You Want To Buy a Home

Have you been saving up to buy a home this year? If so, you know there are a number of expenses involved – from your down payment to closing costs. But did you also know your tax refund can help you pay for some of these expenses? As Credit Karma explains:

“If one of your goals is to stop renting and buy a home, you’ll need to save up for closing costs and a down payment on the mortgage. A tax refund can give you a start on the road to homeownership. If you’ve already started to save, your tax refund could move you down the road faster.”

While how much money you may get in a tax refund is going to vary, it can be encouraging to have a general idea of what’s possible. Here’s what CNET has to say about the average increase people are seeing this year:

“The average refund size is up by 6.1%, from $2,903 for 2023’s tax season through March 24, to $3,081 for this season through March 22.”

Sounds great, right? Remember, your number is going to be different. But if you do get a refund, here are a few examples of how you can use it when buying a home. According to Freddie Mac:

- Saving for a down payment – One of the biggest barriers to homeownership is setting aside enough money for a down payment. You could reach your savings goal even faster by using your tax refund to help.

- Paying for closing costs – Closing costs cover some of the payments you’ll make at closing. They’re generally between 2% and 5% of the total purchase price of the home. You could direct your tax refund toward these closing costs.

- Lowering your mortgage rate – Your lender might give you the option to buy down your mortgage rate. If affordability is tight for you at today’s rates and home prices, this option may be worth exploring. If you qualify for this option, you could pay upfront to have a lower rate on your mortgage.

The best way to get ready to buy a home is to work with a team of trusted real estate professionals who understand the process and what you’ll need to do to be ready to buy.

Bottom Line

Your tax refund can help you reach your savings goal for buying a home. Let’s talk about what you’re looking for, because your home may be more within reach than you think.

Overpricing Your House Could Cost You

Why Overpricing Your House Can Cost You

If you’re trying to sell your house, you may be looking at this spring season as the sweet spot – and you’re not wrong. We’re still in a seller’s market because there are so few homes for sale right now. And historically, this is the time of year when more buyers move. Competition ticks up. That makes this an exciting time to put up that for sale sign.

But while conditions are great for sellers like you, I still want you to be strategic when it comes time to set your asking price. That’s because pricing your house too high may actually cost you in the long run.

The Downside of Overpricing Your House

The asking price for your house sends a message to potential buyers. From the moment they see your listing, the price and the photos are what’s going to make the biggest first impression. And, if it’s priced too high, you may turn people away. They may not even consider seeing your home ‘in person’. As an article from U.S. News Real Estate says:

“Even in a hot market where there are more buyers than houses available for sale, buyers aren’t going to pay attention to a home with an inflated asking price.”

That’s because no homebuyer wants to pay more than they have to, especially not today. Many are already feeling the pinch on their budget due to ongoing home price appreciation and today’s mortgage rates. And if they think your house is overpriced, they may write it off without even stepping foot in the front door, or simply won’t make an offer if they think it’s priced too high.

If that happens, it’s going to take longer to sell. And ideally you don’t want to have to think about doing a price drop to try to re-ignite interest in your house. Why? Some buyers will see the price cut as a red flag and wonder why the price was reduced. Or they’ll think something is wrong with the house the longer it sits. As an article from Forbes explains:

“It’s not only the price of an overpriced home that turns buyers off. There’s also another negative component that kicks in. . . . if your listing just sits there and accumulates days on the market, it will not be a good look. . . . buyers won’t necessarily ask anyone what’s wrong with the home. They’ll just assume that something is indeed wrong, and will skip over the property and view more recent listings.”

Your Agent’s Role in Setting the Right Price

Instead, pricing it at or just below current market value from the start is a much better strategy. So how do you find that ideal asking price? You lean on the pros. Only an agent has the expertise needed to research and figure out the current market value for your home.

I’ll factor in the condition of your house, any upgrades you’ve made, and what other houses like yours are selling for in your area. And I’ll use all of that information to find that target number. The right price will bring in more buyers and make it more likely you’ll see multiple offers too. Plus, when homes are priced right, they still tend to sell quickly.

Bottom Line

Even though you want to bring in top dollar when you sell, setting the asking price too high may deter buyers and slow down the sales process.

Let’s connect to find the right price for your house, so we can maximize your profit and still draw in eager buyers willing to make competitive offers.

The Best Week To List Your Minneapolis House Is Almost Here

When to List Your Home in 2024

Are you thinking about making a move? If so, now may be the perfect time to start the process. That’s because experts say the best week to list your house is just around the corner.

A recent Realtor.com study looked at housing market trends over the past several years (with the exception of 2020, since it was an unusual year), and found the best week to put your house on the market this year is April 14-20:

“Every year, one week stands out from the rest as that perfect stretch of time when it’s great to be a home seller. This year, the week of April 14–20 is the best time to sell—that is, if sellers want to see lots of interest in their homes, sell quickly, and pocket some extra cash, according to Realtor.com® data.”

Here’s why this matters for you. While the spring market is a great time to sell no matter the week, this may be the peak sweet spot. And if you’ve been putting your plans on the back burner and waiting for the right time to act, this could be the nudge you need to make your move happen. As Hannah Jones, Senior Economic Research Analyst at Realtor.com explains:

“The third week of April brings the best combination of housing market factors for sellers. The best week offers higher buyer demand, lower competition [from other sellers], and fewer price reductions than the typical week of the year.”

But, if you want to get in on the action, you’ll need to move quickly and lean on the pros. Your local real estate agent is the perfect go-to when it comes to figuring out a plan to prep your house and get it on the market.

They’ll be able to offer advice to balance your target listing date with what you need to do from a repair and renovation standpoint. And they can walk you through exactly how to prioritize your list so you know what to tackle first.

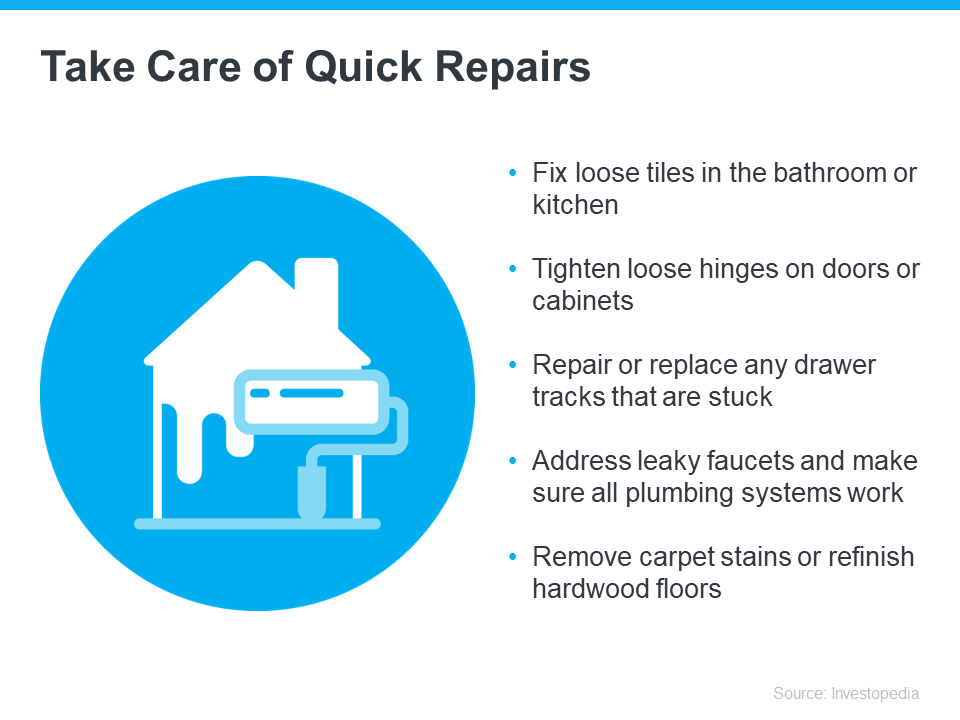

For example, if your house is already in good shape, you’ll be able to really focus in on the smaller things that are easy to do and make a big impact. As an article from Investopedia says:

“You won’t have time for any major renovations, so focus on quick repairs to address things that could deter potential buyers.”

Here are some specific examples from that article:

Just remember, even if you’re not ready to list within the next couple of weeks, that’s okay. The window of opportunity doesn’t close when this week ends. Spring is the peak homebuying season and it’s still a seller’s market, so you’ll be in the driver’s seat all season long.

Bottom Line

Ready to get the ball rolling? Let’s connect and schedule a time to go over your next steps. I’m here to help!

It’s Time To Prepare Your House for a Spring Listing

Prepare Now for a Spring Listing

Prepare your home for the spring market

If you’re thinking of selling your house this spring, now is the perfect time to start getting it ready. With the market gearing up for its busiest time of year, it’ll be important to make sure your house shines bright among the competition.

Here are some valuable tips you can use to get your house market-ready.

Declutter and Organize

First impressions matter, and if your house is a mess, that can easily turn off potential buyers. Before listing, take the time to declutter and organize each room. Decluttering is about more than just tidying up – it’s about creating a sense of space and openness that allows potential buyers to envision themselves living in your home. According to Moving.com:

“Decluttering and organizing your space will go a long way in appealing to potential buyers. . . .decluttering will help the buyers see themselves living in your home. Less clutter inside a home also helps a place appear larger and cleaner, which should attract more buyers.”

Deep Clean Your Kitchen and Bathrooms

The kitchen and bathrooms are focal points for many buyers, and often influence their overall opinion of the house. Ensure these spaces dazzle by giving them a thorough deep cleaning. Pay attention to details like scrubbing grout lines, polishing fixtures, and decluttering countertops. A sparkling kitchen and bathroom can leave a lasting positive impression on potential buyers.

Maintain Your Yard

Your home’s exterior is the first thing potential buyers see, so it’s important to make a good impression from the moment they arrive. A well-maintained yard not only enhances curb appeal, but also shows buyers the home has been well taken care of.

Take the time to spruce up your yard by mowing the lawn, trimming bushes, and clearing away any debris or dead plants. Remember, the goal is to create a welcoming environment that entices buyers to step inside and imagine themselves living there. U.S. News says:

“A beautifully landscaped front yard can elevate an ordinary house into a charming home and will help homes sell faster and for more money.”

Find a Listing Agent

A skilled listing agent is your partner in minimizing stress when selling your home. Lean on your agent for advice on decluttering, staging, and enhancing your home’s appeal to potential buyers. Their insights into market trends and recommendations for reliable contractors and stagers are invaluable. As Realtor.com says:

“A good listing agent will help you price your home . . . recommend a photographer and stager to make it look its best, and put your home on the multiple listing service.”

Bottom Line

By decluttering, deep cleaning, and tidying up your house, you can create a welcoming environment that resonates with buyers and increases your chances of a successful sale. Let’s connect on what you need to do to get your house ready to sell this spring!

The Biweekly Mortgage – Who Needs It?

Have you received an advertisement offering to save you thousands of dollars on your thirty-year mortgage and cut years off your payments? With email spam becoming more pervasive as everyone tries to get rich quick on the Internet, these ads are popping up with troublesome regularity.

Have you received an advertisement offering to save you thousands of dollars on your thirty-year mortgage and cut years off your payments? With email spam becoming more pervasive as everyone tries to get rich quick on the Internet, these ads are popping up with troublesome regularity.

The ads promote a Biweekly Mortgage and for the most part, do not come from a mortgage lender. Exclamation points punctuate practically every claim:

- No closing costs!

- No refinancing!

- No points!

- No credit check!

- No appraisal!

- Save thousands!

- Cut years off your mortgage!

To achieve these wonderful savings all you have to do is allow half of your mortgage payment to be deducted from your checking account every two weeks. It’s easy. Of course, there is a small set-up fee and usually a transaction fee with every automatic deduction.

Essentially, the ads are truthful in almost every respect.

They just want to charge you money for something you can do on your own for free.

The Basics:

Normally, you make twelve mortgage payments a year. Since there are fifty-two weeks in a year, a biweekly mortgage equals 26 half-payments a year. The equivalent would be making thirteen mortgage payments a year instead of twelve. By applying that extra payment directly to the loan balance as a principal reduction, your loan amortizes more quickly, requiring fewer payments.

You save money. The ads are true.

How it Actually Works:

You cannot simply mail in half a payment every two weeks to your mortgage lender. Since they do not accept partial payments for legal and accounting reasons, the mortgage company would just mail your half-payment back to you.

Instead, the biweekly mortgage company is an intermediary between you and your mortgage lender. They automatically debit your checking account every two weeks for half of your mortgage payment then place your funds into a trust account. Basically, this is just a holding account for your money. In another two weeks, there is another automatic deduction from your checking account, and so on. When your mortgage payment is due, your funds are withdrawn from the trust account and forwarded to your mortgage lender.

Since you are placing funds into the trust account faster than your mortgage payments are due, you eventually accumulate enough money to make an extra payment. The way the cycle works, this occurs once a year. he extra payment is applied directly to your principal balance, which causes your loan to amortize faster, pay off more quickly and save you thousands of dollars.

Potential Problems with the Trust Account

Because your funds are held in the trust account until your mortgage payment is due, there are potential dangers. Not only are your funds held in this account, but so are the funds of everyone else enrolled in the biweekly program. That is a lot of money.

Most likely, there will be no problems.

However, if there are accounting errors, mismanagement, or even fraud, your mortgage payment might not get made. The first hint of a problem will probably be a phone call or letter from your mortgage lender, but not until after your payment is already late. Since responsibility for making the payment rests with you and not the biweekly payment company, you may find yourself digging into your personal savings to make the payment directly — even though the biweekly payment company has already collected your funds.

Later you can work out the trust account problem with your biweekly payment company.

The Cost of the Biweekly Mortgage

There is usually a set-up fee that runs between $195 and $350, depending on how much sales commission is paid to the individual or company setting up the account for you. You also pay a transaction fee each time there is an automatic deduction from your checking account and sometimes also when the payment is made to your mortgage lender. There may also be a periodic maintenance fee.

Meanwhile, whoever controls the trust account is earning interest on your money.

Savings of the Biweekly Mortgage

By making principal reductions using the biweekly mortgage program, your mortgage will amortize more quickly, saving you money. How quickly your loan pays off depends on your interest rate and when you begin making the biweekly payments.

On a $100,000 loan at an interest rate of eight percent, your first principal reduction would probably be a year from now. Assuming the principal reduction is equal to one monthly payment ($733.76), you would save $43,852 over the life of the loan and pay it off almost seven years early.

However, you have to deduct from those savings any amounts you paid in set-up, transaction, and maintenance fees.

No-Cost Alternatives to the Biweekly Mortgage

Instead of hiring a company to manage your biweekly payment, you could accomplish essentially the same thing on your own for free. Just take your monthly payment, divide it by twelve, and add that amount to your monthly mortgage payment. Be sure to earmark it as a principal reduction.

The first way you save is that you do not have to pay any fees to anyone. It’s free.

In addition to not paying fees — using the same example as above — your total savings on the mortgage would be $45,904. Plus the loan would be paid off three months quicker than with the biweekly mortgage. The reason you save more is because you are making a principal reduction each month, instead of waiting for funds to accumulate so that you can make one principal reduction a year.

Self-Discipline?

The biweekly mortgage companies claim that homeowners are not disciplined enough to follow through with principal reduction plans on their own. They suggest the reason for setting up the biweekly mortgage enforces discipline upon you, and by doing so, they save you money.

However, in this technologically advanced age, banking online and automatic deductions are readily available. You can set up your own automatic deductions including the additional principal reduction and have it go directly to your mortgage lender. Since the deduction occurs automatically, just like with the biweekly mortgages, self-discipline is not a problem. Once again, you don’t have to pay anyone to do it for you and you save even more money.

Conclusion

The biweekly mortgage plans do not really do anything except move your money around and charge you for it. Plus, even though the danger is negligible, you must trust someone else to hold your money for you. If you can do the very same thing for free, plus save yourself even more money by doing it on your own, why pay someone else?

The biweekly mortgage plan – who needs it?

If your goal is principal reduction and saving money, then it is a good plan. If you do it on your own instead of paying someone else to do it for you, then it is a great plan.

Downsize Your Home Right-Size Your Life

When you’ve lived somewhere for many years, it can be tough to say goodbye. But if you (or a loved one) currently have a home that is bigger than necessary or is too high maintenance, it may be time to trade unused square footage for a smaller, more manageable space.

When you’ve lived somewhere for many years, it can be tough to say goodbye. But if you (or a loved one) currently have a home that is bigger than necessary or is too high maintenance, it may be time to trade unused square footage for a smaller, more manageable space.DESIRED LIFESTYLE

Action item: Grab a pen and take some time to envision what your ideal future might look like. Write down the activities and hobbies you hope to add to your life or continue with going forward, as well as the chores and responsibilities you’d love to drop. We can use those answers to help shape your house hunt.

OPTIMAL DESIGN

Action item: Make a note of your must-keep furniture and other items. Then pull out a measuring tape and write down the dimensions. Once it’s time to visit homes, we’ll have a more accurate sense of what will fit and how much space you’ll need.To get your creative juices flowing, you may also want to flip through some design magazines that specialize in compact living or catalogs that feature space-saving furniture and accessories. If you give us a list of your favorite features, we can use it to pinpoint homes that are a good match.

LONG-TERM ACCESSIBILITY

Action item: Review the checklist below, adapted from the National Institute on Aging’s home safety worksheet, or download the full version from the agency’s website.7 Highlight the items that are most important to you. We can reference these guidelines as we consider potential homes and suggest ways to adapt a property to meet your current or future requirements.

HOME SAFETY CHECKLIST 7

BOTTOMLINE

-

Associated Press (AP) – https://apnews.com/article/lifestyle-f094372b46bae82020c174907eb953c0

-

Healthcare (Basel) – https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10671417/

-

National Poll on Healthy Aging – https://www.healthyagingpoll.org/reports-more/report/older-adults-preparedness-age-place

-

National Council on Aging (NCOA) – https://www.ncoa.org/adviser/medical-alert-systems/downsizing-for-aging-in-place/

-

National Institute of Health (NIH) – https://www.nia.nih.gov/sites/default/files/2023-04/worksheet-home-safety-checklist_1.pdf

4 Tips To Make Your Strongest Offer When Buying a Home

Make a strong offer to buy a home

Are you thinking about buying a home soon? If so, you should know today’s market is competitive in many areas because the number of homes for sale is still low – and that’s leading to multiple-offer scenarios. And moving into the peak homebuying season this spring, this is only expected to ramp up more.

Remember these four tips to make your best offer.

1. Partner with a Real Estate Agent

Rely on a real estate agent who can support your goals. As PODS notes:

“Making an offer on a home without an agent is certainly possible, but having a pro by your side gives you a massive advantage in figuring out what to offer on a house.”

I know the local market areas. I also know what’s worked for other buyers in your area and what sellers may be looking for. That advice can be game changing when you’re deciding what offer to bring to the table.

2. Understand Your Budget

Knowing your numbers is even more important right now. The best way to understand your budget is to work with a lender so you can get pre-approved for a home loan. Doing so helps you be more financially confident and shows sellers you’re serious. That gives you a competitive edge. As Investopedia says:

“. . . sellers have an advantage because of intense buyer demand and a limited number of homes for sale; they may be less likely to consider offers without pre-approval letters.”

3. Make a Strong, but Fair Offer

It’s only natural to want the best deal you can get on a home, especially when affordability is tight. However, submitting an offer that’s too low does have some risks. You don’t want to make an offer that’ll be tossed out as soon as it’s received just to see if it sticks. As Realtor.com explains:

“. . . an offer price that’s significantly lower than the listing price, is often rejected by sellers who feel insulted . . . Most listing agents try to get their sellers to at least enter negotiations with buyers, to counteroffer with a number a little closer to the list price. However, if a seller is offended by a buyer or isn’t taking the buyer seriously, there’s not much you, or the real estate agent, can do.”

The expertise I bring as your agent to this part of the process will help you stay competitive and find a price that’s fair to you and the seller.

4. Trust Your Agent During Negotiations

After you submit your offer, the seller may decide to counter it. When negotiating, it’s smart to understand what matters to the seller. Once you do, being as flexible as you can on things like moving dates or the condition of the house can make your offer more attractive.

As your real estate agent I am your partner in navigating these details. Trust me to lead you through negotiations and help you figure out the best plan. As an article from the National Association of Realtors (NAR) explains:

“There are many factors up for discussion in any real estate transaction—from price to repairs to possession date. A real estate professional who’s representing you will look at the transaction from your perspective, helping you negotiate a purchase agreement that meets your needs . . .”

Bottom Line

In today’s competitive market, let’s work together to find you a home you love and craft a strong offer that stands out.

Why You Want an Agent’s Advice for Your Move in Minnetonka

Why You Want an Agent’s Advice When You Move to Minnetonka

No matter how you slice it, buying or selling a home is a big decision. And when you’re going through any change in your life and you need some guidance, what do you do? You get advice from people who know what they’re talking about.

Moving is no exception. You need insights from the pros to help you feel confident in your decision. Freddie Mac explains it like this:

“As you set out to find the right home for your family, be sure to select experienced, trusted professionals who will help you make informed decisions and avoid pitfalls.”

And while perfect advice isn’t possible – not even from the experts, what you can get is the very best advice out there.

The Power of Expert Advice

For example, let’s say you need an attorney. You start off by finding an expert in the type of law required for your case. Once you do, they won’t immediately tell you how the case is going to end, or how the judge or jury will rule. But what a good attorney can do is walk you through the most effective strategies based on their experience and help you put a plan together. They’ll even use their knowledge to adjust that plan as new information becomes available.

The job of a real estate agent is similar. Just like you can’t find a lawyer to give you perfect advice, you won’t find a real estate professional who can either. That’s because it’s impossible to know everything that’s going to happen throughout your transaction. Their role is to give you the best advice they can.

To do that, an agent will draw on their experience, industry knowledge, and market data. They know the latest trends, the ins and outs of the homebuying and selling processes, and what’s worked for other people in the same situation as you.

With that expertise, a real estate advisor can anticipate what could happen next and work with you to put together a solid plan. Then, they’ll guide you through the process, helping you make decisions along the way. That’s the very definition of getting the best – not perfect – advice. And that’s the power of working with a real estate advisor.

Bottom Line

If you’re looking to buy or sell a home, you want an expert on your side to help you each step of the way. Let’s connect so you have advice you can count on.

A Fixer-Upper Could be Your Perfect Home

Finding Your Perfect Home in a Fixer Upper

If you’re trying to buy a home and are having a hard time finding one you can afford, it may be time to consider a fixer-upper. That’s a house that needs a little elbow grease or some updates, but has good bones. Fixer-uppers can be a really great option if you’re looking to break into the housing market or want to stretch your budget further. According to NerdWallet:

“Buying a fixer-upper can provide a path to homeownership for first-time home buyers or a way for repeat buyers to afford a larger home or a better neighborhood. With the relatively low inventory of homes for sale these days, a move-in ready home can be hard to find, especially if you’re on a budget.”

Since the number of homes for sale is still so low, if you’re only willing to tour homes that have all your dream features, you may be cutting down your options too much. This could make it harder on yourself than necessary. It may be time to cast a wider net.

Sometimes the perfect home is the one you perfect after buying it.

Here’s some information that can help you pinpoint what you truly need so you can be strategic in your home search. First, make a list of all the features you want in a home. From there, work to break those features into categories like this:

- Must-Haves – If a house doesn’t have these features, it won’t work for you and your lifestyle.

- Nice-To-Haves – These are features you’d love to have but can live without. Nice-to-haves aren’t dealbreakers, but if you find a home that hits all the must-haves and some of these, it’s a contender.

- Dream State – This is where you can really think big. Again, these aren’t features you’ll need, but if you find a home in your budget that has all the must-haves, most of the nice-to-haves, and any of these, it’s a clear winner.

Once you’ve sorted your list in a way that works for you, share it with your real estate agent. They’ll help you find homes that deliver on your top needs right now and have the potential to be your dream home with a little bit of sweat equity. Lean on their expertise as you think through what’s possible, what features are easy to change or add, and how to make it happen. According to Progressive:

“Many real estate agents specialize in finding fixer-uppers and have a network of inspectors, contractors, electricians, and the like.”

Your agent can also offer advice on which upgrades and renovations will set you up to get the greatest return on your investment if you ever decide to sell down the line.

Bottom Line

If you haven’t found a home you love that’s in your budget, it may be worth thinking through all your options, including fixer-uppers. Sometimes the perfect home for you is the one you perfect after buying it. To see what’s available in our area, let’s connect.